SREI Infrastructure Finance 9.50% Non-Convertible Debentures (NCDs) – January 2017 Issue

Falling interest rates on bank FDs has resulted in investors hunting for higher yield fixed income options, which in turn has prompted private NBFCs to launch a slew of NCD issues in the last 4-5 months. DHFL, Indiabulls Housing Finance, Reliance Home Finance, SREI Equipment Finance and Muthoot Finance, all have been successful in raising their full quota of required funds, at a much lower rate of interest and in a much shorter period of time as against how it used to happen 2-3 years back at a much higher rate of interest of 11-12%.

To join this bandwagon, SREI Infrastructure Finance Limited (SREI Infra) is launching its second issue of Secured Non-Convertible Debentures (NCDs) from today. These NCDs will carry 9.50% and 9.25% annual rate of interest for a period of 5 years and 3 years respectively. The issue will remain open for around four weeks to close on February 23.

As we analyse it further, let us take a quick look at the salient features of this issue.

Size & Objective of the Issue – Base size of this issue is Rs. 200 crore, with a green-shoe option to retain an additional Rs. 506.64 crore, thus making it a Rs. 706.64 crore issue. The company plans to use at least 75% of the issue proceeds for its lending activities and to repay its existing loans and up to 25% of the proceeds for general corporate purposes.

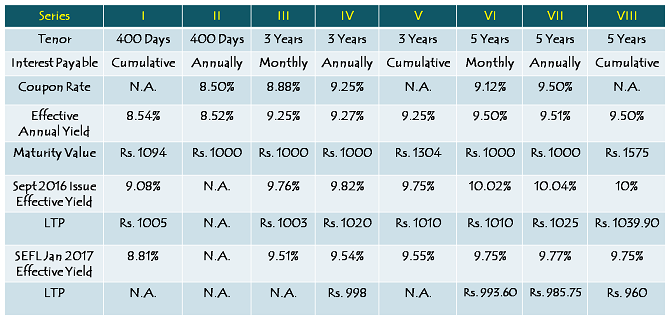

Coupon Rate & Tenor of the Issue – The issue will carry a coupon rate of 9.50% p.a. payable on an annual or cumulative basis and 9.12% p.a. payable on a monthly basis for a period of 5 years (60 months) and 9.25% p.a. payable on an annual or cumulative basis and 8.88% p.a. payable on a monthly basis for a period of 3 years (36 months). The issue will have the option of 400 days also, in which the investors will get 8.50% p.a. on an annual or cumulative basis.

0.25% Additional Coupon for SREI Infra Shareholders, NCD Holders, Senior Citizens & Employees – Existing shareholders and NCD holders of SREI Infra, senior citizens aged more than 60 years of age and the employees of SREI Infra will be offered an additional coupon of 0.25% per annum. Deemed date of allotment will be considered the relevant date for these investors to be eligible for this additional rate of interest.

Minimum Investment – Investors are required to make a minimum investment of Rs. 10,000 i.e. ten NCDs of face value Rs. 1,000 each.

Categories of Investors & Allocation Ratio – The investors have been classified in the following three categories and each category will have the below mentioned percentage fixed in the allotment:

Category I – Institutional Investors – 10% of the issue i.e. Rs. 70.66 crore

Category II – Non-Institutional Investors – 20% of the issue i.e. Rs. 141.33 crore

Category III – Individual & HUF Investors – 70% of the issue i.e. Rs. 494.65 crore

Allotment will be made on a first-come first-served basis, as well as on a date priority basis i.e. on the date of oversubscription, the allotment will be made on a proportionate basis to all the applicants of that day on which it gets oversubscribed.

NRIs Not Allowed – Non-Resident Indians (NRIs), foreign nationals and qualified foreign investors (QFIs) among others are not eligible to invest in this issue.

Credit Rating & Nature of NCDs – Rating agency Brickwork Ratings (BWR) has rated this issue as ‘AA+’. Debt instruments with such a rating are considered to have high degree of safety regarding timely payment of interest and principal. Moreover, these NCDs are ‘Secured’ in nature i.e. in case of any default on its payment of interest or principal, the bondholders will have the right on certain secured assets of SREI Infra.

Listing, Premature Withdrawal & Put/Call Option – These NCDs will be listed on both the stock exchanges i.e. Bombay Stock Exchange (BSE) as well as National Stock Exchange (NSE). The listing will take place within 12 working days after the issue gets closed. Though there is no option of a premature redemption, the investors can sell these bonds on the stock exchanges if NCDs are held in a demat form.

Demat Not Mandatory – Demat account is not mandatory to invest in these NCDs as the investors will have the option to apply for these NCDs in physical or certificate form as well.

TDS – Interest income earned is taxable with these NCDs and the investors are required to pay tax on the interest income as per their respective tax slabs. TDS @ 10% will be deducted if these NCDs are held in physical/certificate form and annual interest income is more than Rs. 5,000. NCDs held in demat mode will not attract any TDS.

Should you invest in SREI Infrastructure Finance NCDs?

Infrastructure financing sector has been facing headwinds for the past many years now. Firstly, many infra projects have been stuck at various stages due to various known and unknown reasons. Loans given for many such projects have become NPAs for infra financing companies, including SREI Infra. Secondly, as the economy is still struggling to have a healthy revival, demand for fresh loans as well has not revived. So, till the time we see this cyclical downtrend ending, we should not have high hopes from infra financing companies.

Moreover, as mentioned in my earlier reviews as well, these NCD issues by private companies offering 8.50% to 9.50% are not worth taking risk for me. Investors in the 30% tax bracket would earn 6.56% post-tax annual returns with 5-year NCDs. As you can check from the table above, already listed NCDs of SREI Infra or SREI Equipment Finance are already trading at a yield to maturity (YTM) higher than interest rates offered in this issue. So, it is better to buy their NCDs from the secondary markets.

If I am ready to bear some risk with my money, I would rather invest in equity mutual funds and hope for higher returns as against these NCDs with which though interest income is fixed, but also exists a remote risk of losing my principal as well in case the company goes bankrupt. However, risk-averse investors who are fairly confident about the operational efficiency of SREI Infra’s management and those who cannot take the volatility in returns of equity mutual funds or investors in the lower tax brackets can consider investing in these NCDs.